A Review of the Mid-term Performance of Hang Lung Properties, Wharf and Swire Properties

August 28,2021

Through a summary of the performance of the three commercial property developers - Wharf (HK.00004), Swire Properties (HK.01972) and Hang Lung Properties (HK: 00101) - in the first half of 2021, Luxe.CO explored the latest developments in Chinaтs high-end retail industry in the post-epidemic era.

Wharf

In the first half of 2021, Wharfтs revenue had grown by 122% to HKD 12.337 billion compared to the same period of 2020. The company had also reversed a deficit of HKD 1.741 billion in net profit attributable to its parent company to a surplus of HKD 1.038 billion.

Driven by luxury sales, retail sales had maintained the growth momentum. Income from investment properties in Mainland China had grown by 45% to HKD 2.677 billion. Meanwhile, due to the oversupply of retail space, many property owners would rather pay a high price to compete for a few desired brands.

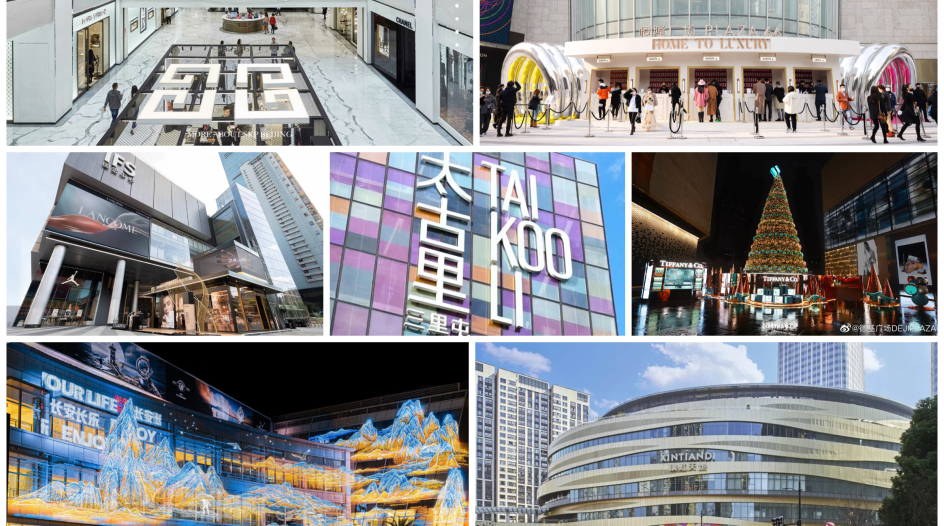

Wharfтs shopping centers in Mainland China include: Changsha IFS, Chengdu IFS, Chongqing IFS, Shanghai Times Square, Wheelock Square, Chongqing Times Square, Dalian Times Square, Times Outlets Changsha and Times Outlets Chengdu.

The revenue of Changsha IFS had grown by 90%. It had more than 370 tenants and an occupancy rate of 99%. The revenue of Chengdu IFS, a landmark in West China, had grown by 45%. It had an occupancy rate of 96%. It had ranked many times among the top ten shopping malls in Mainland China in terms of sales.

Swire Properties

Swire Properties generated a revenue of HKD 9.068 billion and a net profit attributable to its parent company of HKD 1.984 billion in the first half of 2021, an increase of 38% and 92.8%, respectively, over the same period of 2020.

Five of the most important properties of the company in Mainland China are TAIKOO LI SANLITUN, Beijing, INDIGO, Beijing, HKRI TAIKOO HUI, Shanghai, Sino-Ocean TAIKOO LI Chengdu and TAIKOO HUI Guangzhou. They had all produced a great deal of profit and generated strong demand. Its occupancy rate had remained high and foot traffic and sales had grown remarkably. The total rental income from retail properties of the company in Mainland China had grew by 40% to HKD 1.538 billion.

Specifically, retail sales of TAIKOO LI SANLITUN had grown by 85%. The western area of TAIKOO LI SANLITUN has been renovated as an extension of this business complex, which was completed in June 2021 and is expected to open later this year. TAIKOO HUI Guangzhou had increased its retail sales by 88 %, and had also announced full use of renewable electricity. Retail sales of Sino-Ocean TAIKOO LI Chengdu had grown by 66% and INDIGO 6%. TAIKOO LI Qiantan, Shanghai, is expected to open in September 2021.

Hang Lung Properties

In the first half of 2021, Hang Lung Propertiesт revenue and net profit attributable to its parent company had grown by 19% and 11% to HKD 4.975 billion and HKD 2.2 billion, respectively, compared to the same period of 2020.

Its rental income in Mainland China had grown by 45% to a record-high of HKD 3.295 billion, which accounted for more than two thirds of its total income. Shanghai Hang Lung Plaza and Grand Gateway 66 were still the most lucrative projects of the company in Mainland China, which generated a rental income of HKD 874 million and HKD 565 million, respectively.

Phenomenal sales growth in the 10 shopping malls of the company in Mainland China had fueled the rise in the rental income of its property portfolios in Mainland China. Since April 2020, the sales of the many luxury brands that were renting its retail space had been rising sharply and continuously. The overall tenant sales had more than doubled and grown by 10% compared with the first half and second half of 2020, respectively.

Specifically, retail sales of Shanghai Hang Lung Plaza, Grand Gateway 66, Shenyang Hang Lung Plaza, Wuxi Hang Lung Plaza, Dilian Hang Lung Plaza and Kunming Hang Lung Plaza had grown by 101%, 116%, 65%, 190%, 80% and 72%, respectively.

| Image source: Chengdu IFS, Swire Properties, Hang Lung Properties

| Writer: Binrong Jing, Jiaqi Wang

Comments